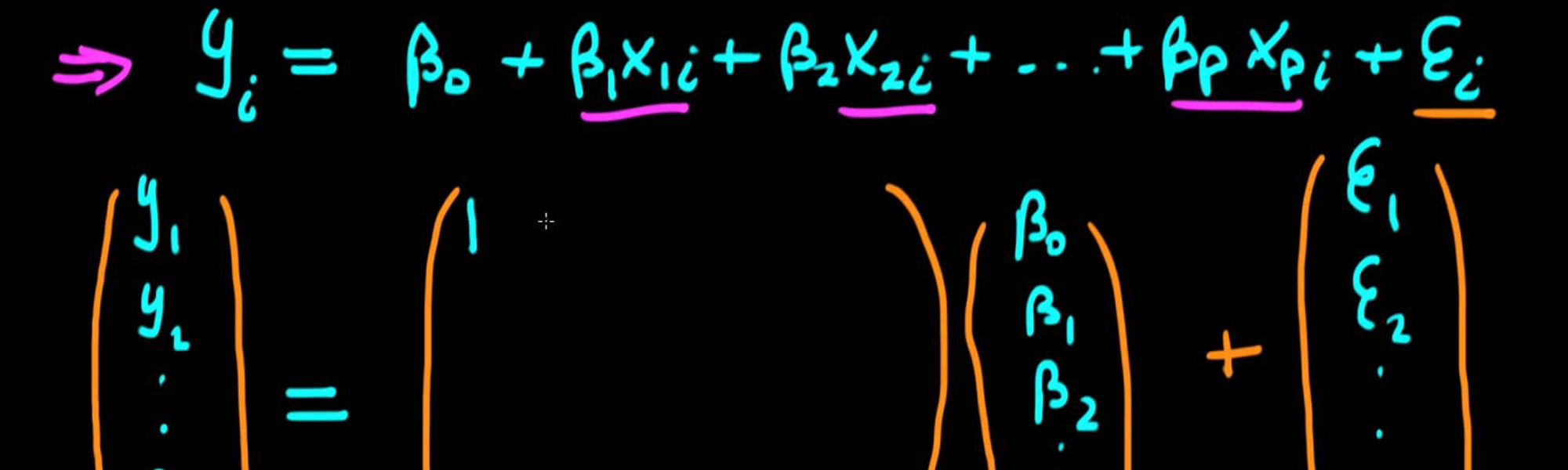

This letter proposes a simple test for the linearity of a time series. We compare the small and large samples properties of the suggested test via Monte Carlo techniques with well known time domain linearity tests. Our results suggest that the suggested test over performs the power of the other competitive tests in small samples.

In this paper we investigate the effects of temporal aggregation and systematic sampling using some well known linear and nonlinear Granger causality tests.

This short paper demonstrates that the use of temporally aggregated data may affect the power and the size of the well known the Ramsey's (1969) RESET test.

This paper examines the existence of a linear or nonlinear interaction between the Advance/Decline ratio index and the returns of the Athens General Index.

In this paper, we investigate the implications of measurement errors in the daily published stock prices on the creation and management of efficient portfolios.

This paper investigates the existence of any linear or non-linear diachronic relationship between the financial newspapers circulations and the General Index of the Athens Stocks Exchange (ASE).

A variety of standard forecasting accuracy criteria and one suggestion are applied to evaluate the OECD's macroeconomic forecasts for Greece for the aggregate demand and output, the GDP implicit price deflator, the investment, the imports and the exports of goods and services.

This paper examines the strategy of investing in selected East European stock markets: The Czech Republic, Hungary, and Poland.

In this paper, we examine the effects of data collection frequency on the computation of the Consumer Price Index (CPI).

This short paper demonstrates the effects of using missing data on the power of the well-known Hausman (1978) test for simultaneity in structural econometric models.

This short paper examines the nonlinear interaction between mutual fund flows and stock returns in Greece. We investigate the possibility of a nonlinear causality mechanism through which mutual funds flows may affect stock returns and vice versa.

In this short paper a Gamma distributed lags model is used to study the diachronic responses between the actual data and the forecasts supplied by OECD the last 27 years for the case of the Greek Economy.

A crucial aspect of empirical research based on ARIMA(p,q) model is the choice of the appropriate lag order. Several criteria have been used in order to identify the appropriate order of a ARIMA(p,q) process. In this paper we investigate the effects of using a variation of selection criteria under different temporal aggregation levels.

This letter proposes a simple test for the linearity of a time series. We compare the small and large samples properties of the suggested test via Monte Carlo techniques with well known time domain linearity tests.

This paper is using simple nonlinearity tests to provide evidence of a positive and significant causal relationship going from stock market development to economic growth in Greece during the last 10 years.

In this paper we test the effects of temporal aggregation (disaggregation) on the efficiency of portfolio construction using the mean variance optimization approach

Join the notification list of the Department of Economics.